Uttarakhand Budget Analysis 2020-21

The Chief Minister, Mr. Trivendra Singh Rawat, presented the Budget for Uttarakhand for the financial year 2020-21 on March 4, 2020.

Budget Highlights

- The Gross State Domestic Product of Uttarakhand for 2020-21 (at current prices) is projected to be Rs 2,93,488 crore. This is a 9.5% increase over the revised estimate for 2019-20.

- Total expenditure for 2020-21 is estimated to be Rs 53,527 crore, a 18.7% increase over the revised estimate of 2019-20. In 2019-20, total expenditure is estimated to decrease by 7.4% (Rs 3,582 crore) from the budget estimate for the year (Rs 48,664 crore).

- Total receipts (excluding borrowings) for 2020-21 are estimated to be Rs 42,474 crore, an increase of 19.5% as compared to the revised estimate of 2019-20. In 2019-20, total receipts (excluding borrowings) are estimated to fall short of the budgeted estimate by Rs 3,457 crore (8.9% of the budgeted estimate).

- Revenue surplus for 2020-21 is targeted at Rs 50 crore, or 0.02% of the Gross State Domestic Product (GSDP). Fiscal deficit is targeted at Rs 7,550 crore (2.57% of GSDP). In 2019-20, the fiscal deficit is estimated to be Rs 6,673 crore (2.49% of GSDP).

- In 2020-21, the sectors of Irrigation and Water Supply, Sanitation, Housing and Urban Development (70%), Welfare of SC/ST/OBC and Minorities (57%), Social Welfare and Nutrition (29%), and Health and Family Welfare (29%) saw the highest increase in allocations over the revised estimate of previous year.

Policy Highlights

- Agriculture: Krishi Utpadan Lagat Sarvekshan Yojana will be started for providing minimum support price for crops such as mandua, sanwa, urad, ghat and masoor. A provision of Rs 2,300 crore has been made for payment of wheat and paddy procured from farmers in 2020-21. Rs 240 crore has been allocated towards assistance to sugar mills for clearing dues of sugarcane farmers.

- Education, Skills and Employment: Government will ensure construction of buildings in all government colleges in the state by 2022. Salary for guest teachers in universities will be increased from Rs 25,000 to Rs 35,000. Mukhyamantri Shikshuta Yojana will be started for learning new work-related skills in different sectors. Mukhyamantri Swarojgar Yojana and Mukhyamantri Palayan Roktham Yojana will be started for generating self-employment opportunities and preventing migration from the state.

- Health and social welfare: Approximately Rs 300 crore has been allocated for establishment of a medical college in Haldwani, Almora and Doon. Mukhyamantri Saubhagyaati Yojana will be started for preventing decline in sex-ratio by providing kits to mothers on birth of a girl child in first delivery. Pension for old-age, dependent widows and disabled to be increased from Rs 1,000 per month to Rs 1,200 per month.

| Uttarakhand’s EconomyGSDP: The growth rate of Uttarakhand’s GSDP (at constant prices) is estimated to be 6.9% in 2018-19, a decline from the 9.8% growth rate in 2016-17, and 7.8% growth rate in 2017-18. Sectors: Agriculture, Industry, and Services are estimated to contribute 10%, 52%, and 38%, respectively to the state’s economy in 2019-20. Both agriculture and industry sectors have seen a decline in their growth over the last few years. Unemployment: According to the Periodic Labour Force Survey (2017-18), Uttarakhand had an unemployment rate of 7.6%, compared to the all-India unemployment rate of 6.1%. The female unemployment rate in Uttarakhand is 10.7%, which is much higher than the all-India female unemployment rate of 5.7%. | Figure 1: Growth in GSDP and sectors in Uttarakhand (year-on-year, at 2011-12 constant prices)Sources: Uttarakhand MTFP Statement 2020-21; PRS. Note: Industry includes manufacturing and construction. Figures for 2018-19 are Advanced Estimates. |

Budget Estimates for 2020-21

- The total expenditure in 2020-21 is targeted at Rs 53,527 crore. This is 18.7% higher than the revised estimates of 2019-20. This expenditure is proposed to be met through receipts (other than borrowings) of Rs 42,474 crore and borrowings of Rs 9,950 crore. Total receipts for 2020-21 (other than borrowings) are expected to be 19.5% higher than the revised estimate of 2019-20. However, they are estimated to fall short of the budgeted estimate by Rs 3,457 crore (8.9% of the budgeted estimate).

Table 1: Budget 2020-21 – Key figures (in Rs crore)

| Items | 2018-19 Actuals | 2019-20 Budgeted | 2019-20 Revised | % change from BE 2019-20 to RE 2019-20 | 2020-21 Budgeted | % change from RE 2019-20 to BE 2020-21 |

| Total Expenditure | 48,794 | 48,664 | 45,082 | -7.4% | 53,527 | 18.7% |

| A. Receipts (except borrowings) | 31,243 | 38,989 | 35,532 | -8.9% | 42,474 | 19.5% |

| B. Borrowings | 15,448 | 9,690 | 6,490 | -33.0% | 9,950 | 53.3% |

| Total Receipts (A+B) | 46,691 | 48,679 | 42,022 | -13.7% | 52,424 | 24.8% |

| Revenue Balance | -980 | 23 | 21 | -8.3% | 50 | 137.6% |

| As % of GSDP | -0.40% | 0.01% | 0.01% | 0.02% | ||

| Fiscal Deficit | 7,321 | 6,798 | 6,673 | -1.8% | 7,550 | 13.1% |

| As % of GSDP | 2.98% | 2.58% | 2.49% | 2.57% | ||

| Primary Deficit | 2,846 | 1,466 | 1,536 | 4.8% | 1,658 | 7.9% |

| As % of GSDP | 1.16% | 0.56% | 0.57% | 0.56% |

Notes: BE is Budget Estimate; RE is Revised Estimate. Positive numbers for revenue balance indicate revenue surplus, negative numbers indicate revenue deficit. GSDP for 2020-21 is Rs 2,93,488 crore. GSDP for 2019-20 BE and 2019-20 RE are Rs 2,63,233 crore and Rs 2,68,025 crore, respectively.

Sources: Uttarakhand Annual Financial Statement 2020-21, Uttarakhand Medium Term Fiscal Policy Statement 2020-21; PRS.

Expenditure in 2020-21

| Debt ServicingIn 2020-21, Uttarakhand is expected to spend Rs 9,396 crore on servicing its debt. This is 17% higher than the revised estimates of 2019-20. This includes Rs 3,503 crore towards repaying loans, and Rs 5,892 crore towards making interest payments. |

- Capital expenditure for 2020-21 is proposed to be Rs 11,137 crore, which is an increase of 16% over the revised estimates of 2019-20.

- Capital expenditure includes expenditure affecting the assets and liabilities of the state, such as: (i) capital outlay, i.e. expenditure which leads to creation of assets (such as bridges and hospitals), and (ii) repayment and grant of loans by the state government.

- Uttarakhand’s capital outlay for 2020-21 is estimated to be Rs 7,383 crore, which is 13.7% higher than the revised estimate of 2019-20. For the year 2019-20, the revised estimate for capital outlay is 1.2% lower than the budget estimate. In 2020-21, 22% of the total capital outlay is towards Transport, and 19% is towards Rural Development and Water Supply, Sanitation, Housing and Urban Development, each.

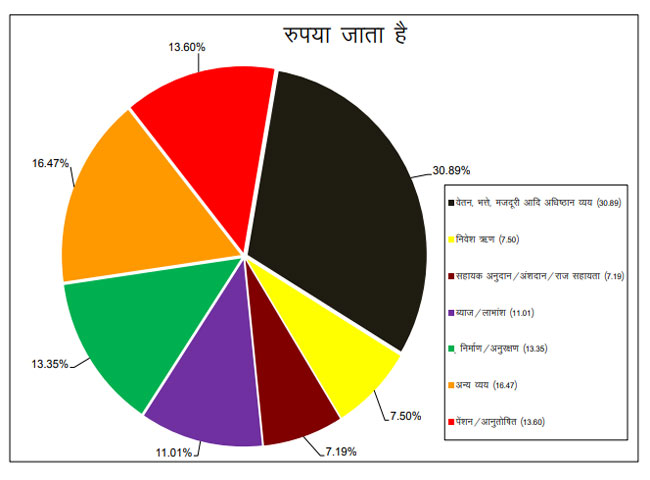

- Revenue expenditure for 2020-21 is proposed to be Rs 42,390 crore, which is an increase of 19.5% over the revised estimates of 2019-20. This expenditure includes payment of salaries, pension, and interest etc.

Table 2: Expenditure budget 2020-21 (in Rs crore)

| Items | 2018-19 Actuals | 2019-20 Budgeted | 2019-20 Revised | % change from BE 2019-20 to RE 2019-20 | 2020-21 Budgeted | % change from RE 2019-20 to BE 2020-21 |

| Capital Expenditure | 16,598 | 9,731 | 9,600 | -1.4% | 11,137 | 16.0% |

| of which Capital Outlay | 6,184 | 6,572 | 6,494 | -1.2% | 7,383 | 13.7% |

| Revenue Expenditure | 32,196 | 38,933 | 35,482 | -8.9% | 42,390 | 19.5% |

| Total Expenditure | 48,794 | 48,664 | 45,082 | -7.4% | 53,527 | 18.7% |

| A. Debt Repayment | 10,230 | 2,876 | 2,876 | 0.0% | 3,503 | 21.8% |

| B. Interest Payments | 4,475 | 5,332 | 5,137 | -3.7% | 5,892 | 14.7% |

| Debt Servicing (A+B) | 14,705 | 8,209 | 8,014 | -2.4% | 9,396 | 17.2% |

Note: Capital outlay denotes expenditure which leads to creation of assets. BE is Budget Estimate; RE is Revised Estimate.

Sources: Uttarakhand Annual Financial Statement 2020-21; PRS.

Sectoral expenditure in 2020-21

The sectors listed below account for 60% of the total budgeted expenditure of Uttarakhand in 2020-21. A comparison of Uttarakhand’s expenditure on key sectors with that by other states can be found in Annexure 1.

Table 3: Sector-wise expenditure for Uttarakhand Budget 2020-21 (in Rs crore)

| Sector | 2018-19Actuals | 2019-20Budgeted | 2019-20Revised | 2020-21Budgeted | % change from RE 2019-20 to BE 2020-21 | Budget provisions for 2020-21 |

| Education, Sports, Arts, and Culture | 7,438 | 8,758 | 7,802 | 9,385 | 20% | Rs 3,131 crore and Rs 4,737 crore have been allocated towards elementary education and secondary education, respectively. Rs 620 crore has been allocated towards higher education. |

| Agriculture and allied activities | 3,483 | 3,325 | 2,869 | 3,401 | 19% | Rs 240 crore has been allocated towards assistance to sugar mills for clearing dues of sugarcane farmers. |

| Rural Development | 3,103 | 3,154 | 2,910 | 3,217 | 11% | Rs 1,072 crore has been allocated for the Pradhan Mantri Gram Sadak Yojana and Rs 267 crore has been allocated towards MGNREGS. |

| Water Supply, Sanitation, Housing and Urban Development | 1,267 | 1,879 | 1,838 | 3,121 | 70% | Rs 134 crore and Rs 123 crore have been allocated towards the Jal Jeevan Mission and Smart City Missions, respectively. |

| Social Welfare and Nutrition | 1,971 | 2,599 | 2,136 | 2,750 | 29% | Rs 505 crore has been allocated towards the Integrated Child Development Scheme. |

| Health and Family Welfare | 2,096 | 2,643 | 2,082 | 2,680 | 29% | Rs 381 crore has been allocated for the National Health Mission. Rs 100 crore have been allocated for the Atal Ayushman Uttarakhand Yojana. |

| Transport | 1,686 | 1,716 | 1,876 | 2,123 | 13% | Rs 295 crore has been allocated for land acquisition for developing Jolly Grant airport, Dehradun into an international airport. |

| Police | 1,794 | 1,894 | 1,775 | 2,094 | 18% | Rs 1,196 crore has been allocated towards the District Police. |

| Public Works | 919 | 1,281 | 1,024 | 1,201 | 17% | Rs 597 crore has been allocated for capital outlay on public works. |

| % of total expenditure | 62% | 60% | 58% | 60% |

Sources: Uttarakhand Budget Speech, Annual Financial Statement and Demand for Grants 2020-21; PRS.

Committed expenditure: Committed expenditure of a state typically includes expenditure on payment of salaries, pensions, and interest. A larger proportion of budget allocated for committed expenditure items limits the state’s flexibility to decide on other expenditure priorities such as capital investments. In 2020-21, the state is estimated to spend Rs 28,104 crore on committed expenditure, i.e. payment of salaries, pensions, and interest. This is 18% higher than the revised estimate of 2019-20 (Rs 23,816 crore). Committed liabilities form nearly two-third (66%) of state’s revenue receipts. This implies that the state has 34% of its revenue receipts left for all other expenditure. Any additional expenditure will be met by the state through borrowings.

Table 4: Committed Expenditure for the state in 2020-21 (in Rs crore)

| Item | 2018-19 Actuals | 2019-20 Budgeted | 2019-20 Revised | % change from BE 2019-20 to RE 2019-20 | 2020-21 Budgeted | % change from RE 2019-20 to BE 2020-21 |

| Salaries | 12,900 | 14,514 | 12,937 | -10.9% | 15,907 | 23.0% |

| Pensions | 5,396 | 5,943 | 5,743 | -3.4% | 6,305 | 9.8% |

| Interest | 4,475 | 5,332 | 5,137 | -3.7% | 5,892 | 14.7% |

| Committed Expenditure | 22,771 | 25,789 | 23,816 | -7.6% | 28,104 | 18.0% |

Sources: Uttarakhand Annual Financial Statement 2020-21; PRS.

Receipts in 2020-21

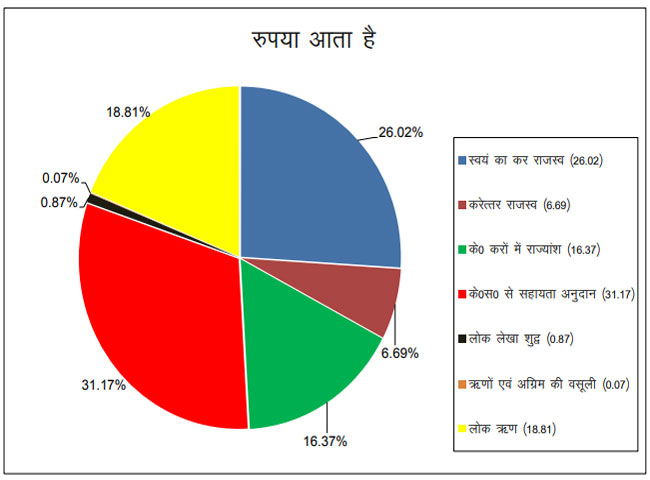

- The total revenue receipts for 2020-21 are estimated to be Rs 42,439 crore, an increase of 19.5% over the revised estimate of 2019-20. Of this, Rs 17,300 crore (41% of the revenue receipts) will be raised through state’s own resources, and Rs 25,139 crore (59% of the revenue receipts) will be in the form of central transfers, i.e. state’s share in central taxes and grants-in-aid from the central government.

- Devolution: In 2020-21, receipts from the state’s share in central taxes are estimated to increase by 15.1% over the 2019-20 revised estimate. However, in 2019-20, devolution is estimated to decrease by 15.4% to Rs 7,521 crore as compared to the budgeted estimate. This may be due to a 19% cut in the union budget for devolution to states, from Rs 8,09,133 crore at the budgeted stage to Rs 6,56,046 crore at the revised stage. Annexure 2 outlines the major recommendations of the 15th Finance Commission for the year 2020-21, including the revised share of Uttarakhand and other states in central government’s tax revenue.

Table 5: Break up of state government receipts (Rs crore)

| Items | 2018-19 Actuals | 2019-20 Budgeted | 2019-20 Revised | % change from BE 2019-20 to RE 2019-20 | 2020-21 Budgeted | % change from RE 2019-20 to BE 2020-21 |

| State’s Own Tax | 12,188 | 14,737 | 12,449 | -15.5% | 13,761 | 10.5% |

| State’s Own Non-Tax | 3,310 | 4,255 | 4,942 | 16.2% | 3,539 | -28.4% |

| Share in Central Taxes | 8,012 | 8,885 | 7,521 | -15.4% | 8,657 | 15.1% |

| Grants-in-aid from Centre | 7,707 | 11,079 | 10,591 | -4.4% | 16,482 | 55.6% |

| Total Revenue Receipts | 31,216 | 38,955 | 35,503 | -8.9% | 42,439 | 19.5% |

| Borrowings | 15,448 | 9,690 | 6,490 | -33.0% | 9,950 | 53.3% |

| Other receipts | 27 | 34 | 29 | -13.3% | 35 | 17.5% |

| Total Capital Receipts | 15,475 | 9,724 | 6,519 | -33.0% | 9,985 | 53.2% |

| Total Receipts | 46,691 | 48,679 | 42,022 | -13.7% | 52,424 | 24.8% |

Sources: Uttarakhand Annual Financial Statement 2020-21; PRS.

- Own tax revenue: Total own tax revenue of Uttarakhand is estimated to be Rs 13,761 crore in 2020-21 (32% of revenue receipts). This is 10.5% higher than the 2019-20 revised estimate. The state’s own tax to GSDP ratio is targeted at 4.7% in 2020-21, which is slightly higher than the revised estimate of 4.6% in 2019-20. This implies that growth in state’s own tax collections is estimated to be slightly higher than its economic growth.

Table 6: Major sources of state’s own-tax revenue (in Rs crore)

| Items | 2018-19 Actuals | 2019-20Budgeted | 2019-20 Revised | % change from BE 19-20 to RE 19-20 | 2020-21 Budgeted | % change from RE 19-20 to BE 20-21 | % of Revenue Receipts in 20-21 |

| State GST | 4,802 | 6,256 | 4,918 | -21.4% | 5,386 | 9.5% | 12.7% |

| State Excise Duty | 2,871 | 3,048 | 3,048 | 0.0% | 3,400 | 11.6% | 8.0% |

| Sales Tax and VAT | 1,883 | 2,353 | 1,813 | -22.9% | 1,970 | 8.6% | 4.6% |

| Stamps Duty and Registration Fees | 1,015 | 1,341 | 1,151 | -14.2% | 1,249 | 8.6% | 2.9% |

| Taxes on Vehicles | 909 | 965 | 965 | 0.0% | 980 | 1.6% | 2.3% |

| Taxes and Duties on Electricity | 506 | 440 | 220 | -50.0% | 500 | 127.2% | 1.2% |

| Land Revenue | 34 | 35 | 35 | 0.0% | 26 | -25.9% | 0.1% |

| GST Compensation Grants | 2,037 | 3,017 | 3,017 | 0.0% | 3,571 | 18.3% | 8.4% |

Sources: Uttarakhand Annual Financial Statement 2020-21, Uttarakhand Detailed Revenue Receipts 2020-21; PRS.

| State Goods and Services Tax (SGST) is the largest component of the state’s tax revenue. It is expected to generate Rs 5,386 crore in 2020-21. This is a 9.5% increase from the revised estimate of 2019-20. SGST comprises 12.7% of the revenue receipts for the year 2020-21. In 2020-21, Uttarakhand is expected to generate Rs 3,400 crore from state excise and Rs 1,970 crore from sales tax. The revenue generated from these items is estimated to exceed the revised estimates of 2019-20 by 11.6%, and 8.6%, respectively. | GST Compensation: The GST (Compensation to States) Act, 2017 guarantees states compensation for five years (till 2022) for any revenue loss arising due to GST implementation. The Act guarantees states a 14% annual growth on their revenue which was subsumed under GST. If the GST revenue of a state does not match the guaranteed growth, compensation grants are provided to meet the shortfall.Uttarakhand has estimated GST compensation grants of Rs 3,571 crore for 2020-21, which is a 18% increase over the revised estimate of 2019-20 (Rs 3,017 crore). Note that an increase in the compensation requirement of the state reflects a further decrease in the GST revenue growth rate, as compared to the 14% growth proposed under the Act. |

Deficits, Debts and FRBM Targets for 2020-21

The Uttarakhand Fiscal Responsibility and Budget Management Act, 2005 provides annual targets to progressively reduce the outstanding liabilities, revenue deficit, and fiscal deficit of the state government.

| Revenue deficit to revenue surplus: In 2019-20, the state is estimated to have a revenue surplus of Rs 21 crore. This is a change in the state’s revenue balance from a revenue deficit of Rs 980 crore in 2018-19.This is because of an estimated increase of 13.7% in revenue receipts in 2019-20, as compared to the previous year. In comparison, the state’s revenue expenditure is estimated to increase by 10.2% during the same period. |

Revenue deficit: It is the excess of revenue expenditure over revenue receipts. A revenue deficit implies that the government needs to borrow in order to finance its expenses which do not create capital assets. The budget estimates a revenue surplus of Rs 50 crore (or 0.02% of GSDP) in 2020-21. This implies that revenue receipts are expected to be slightly higher than revenue expenditure, resulting in a revenue surplus. In 2019-20, the state had estimated a revenue surplus of Rs 21 crore, as per the revised estimates.

Fiscal deficit: It is the excess of total expenditure over total receipts. This gap is filled by borrowings by the state government and leads to an increase in total liabilities. In 2020-21, fiscal deficit is estimated to be Rs 7,550 crore, which is 2.6% of the GSDP. In 2019-20, as per the revised figures, the fiscal deficit is estimated at Rs 6,673 crore or 2.5% of GSDP. These estimates are within than the 3% limit as per the FRBM Act.

Outstanding Liabilities: Outstanding liabilities is the accumulation of borrowings over the years. In 2020-21, the state’s outstanding liabilities are expected to be 24.4% of the GSDP. This is higher than the 20% limit suggested by the FRBM Review Committee in 2017 for the cumulative debt of states. The budget also estimates targets of outstanding liabilities for the coming years. It has estimated the outstanding liabilities to increase to 26.3% of the GSDP by 2023-24.

Table 7: Budget targets for deficits for Uttarakhand in 2020-21 (% of GSDP)

| Year | Revenue | Fiscal | Outstanding Liabilities |

| Deficit (-)/Surplus (+) | Deficit (-)/Surplus (+) | ||

| 2018-19 (Actual) | -0.4% | -3.0% | 23.6% |

| 2019-20 (RE) | 0.0% | -2.5% | 24.1% |

| 2020-21 | 0.0% | -2.6% | 24.4% |

| 2021-22 | 0.0% | -2.7% | 24.9% |

| 2022-23 | 0.0% | -2.8% | 25.6% |

| 2023-24 | 0.0% | -3.0% | 26.3% |

Sources: Uttarakhand Budget Documents 2020-21

Note: RE means Revised Estimate. Figures for 2020-21, 2021-22, 2022-23 and 2023-24 are budget targets.

Figures 2 and 3 show the trend in deficits and outstanding liabilities targets from 2018-19 to 2022-23.

| Figure 2: Revenue and Fiscal Balance(as % of GSDP)Sources: Uttarakhand MTFP Statement 2020-21; PRS. Note: Positive numbers indicate surplus, negative indicate deficit. Figures for 2020-21, 2021-22 and 2022-23 are budget targets. | Figure 3: Outstanding debt (as % of GSDP)Sources: Uttarakhand MTFP Statement 2020-21; PRS. Note: RE is Revised Estimate. Figures for 2020-21, 2021-22 and 2022-23 are budget targets. |

Annexure 1: Comparison of states’ expenditure on key sectors

The graphs below compare Uttarakhand’s expenditure on six key sectors as a proportion of its total expenditure (revenue expenditure + capital outlay) on all sectors. The average for a sector indicates the average expenditure in that sector by 29 states as per their budget estimates of 2019-20.[1]

- Education: Uttarakhand has allocated 18.9% of its expenditure on education in 2020-21. This is higher than the average budget allocation (15.9%) for education by states (using 2019-20 BE).

- Health: Uttarakhand has allocated 5.4% of its total expenditure on health, which is slightly higher than the average allocation for health by states (5.3%).

- Agriculture and allied activities: The state has allocated 6.8% of its total budget towards agriculture and allied activities. This is slightly lower than the average allocations by states (7.1%).

- Rural development: Uttarakhand has allocated 6.5% of its expenditure on rural development. This is slightly higher than the average allocation for rural development by states (6.2%).

- Police: Uttarakhand has allocated 4.2% of its total expenditure on police, which is slightly higher than the average allocation for police by states (4.1%).

- Roads and bridges: Uttarakhand has allocated 3.1% of its total expenditure on roads and bridges, which is lower than the average allocation by states (4.2%).

Note: 2018-19, 2019-20 (BE), 2019-20 (RE), and 2020-21 (BE) figures are for Uttarakhand.

Source: Annual Financial Statement (2019-20 and 2020-21), various state budgets; PRS.

Annexure 2: 15th Finance Commission’s recommendations for 2020-21

The 15th Finance Commission’s (15th FC) report for the financial year 2020-21 was tabled in Parliament on February 1, 2020. The 15th FC recommended a 41% share for states in the central government’s tax revenue in 2020-21, a 1% decrease from the 42% share recommended by the 14th FC (2015-20). The 1% decrease is to provide funds to the newly formed union territories of Jammu and Kashmir, and Ladakh from the share of the central government. The 15th FC also proposed revised criteria for determining the share of individual states.

Table 8 shows the share of states in the central government’s tax revenue[1], as per the recommendations of the 14th FC for 2015-20 and the 15th FC for 2020-21. The 15th FC has recommended a 0.45% share for Uttarakhand in the centre’s tax revenue for 2020-21 (a marginal increase from the 0.44% share recommended by the 14th FC for 2015-20). This implies that out of every Rs 100 of centre’s tax revenue in 2020-21, Uttarakhand will receive Rs 0.45. Table 8 also shows the estimated devolution to states by the centre for 2019-20 and 2020-21 (in Rs crore).

Table 8: Share of states in Centre’s taxes (recommendations by 14th and 15th Finance Commission)

| State | Share of states in centre’s tax revenue | Devolution to states by the centre | ||||

| 14th FC (2015-20) | 15th FC (2020-21) | % change | 2019-20 RE | 2020-21 BE | % change | |

| Andhra Pradesh | 1.81 | 1.69 | -7% | 28,242 | 32,238 | 14% |

| Arunachal Pradesh | 0.58 | 0.72 | 24% | 8,988 | 13,802 | 54% |

| Assam | 1.39 | 1.28 | -8% | 21,721 | 24,553 | 13% |

| Bihar | 4.06 | 4.13 | 2% | 63,406 | 78,896 | 24% |

| Chhattisgarh | 1.29 | 1.4 | 9% | 20,206 | 26,803 | 33% |

| Goa | 0.16 | 0.16 | 0% | 2,480 | 3,027 | 22% |

| Gujarat | 1.3 | 1.39 | 7% | 20,232 | 26,646 | 32% |

| Haryana | 0.46 | 0.44 | -4% | 7,112 | 8,485 | 19% |

| Himachal Pradesh | 0.3 | 0.33 | 10% | 4,678 | 6,266 | 34% |

| Jammu and Kashmir | 0.78 | – | – | 12,171 | – | – |

| Jharkhand | 1.32 | 1.36 | 3% | 20,593 | 25,980 | 26% |

| Karnataka | 1.98 | 1.49 | -25% | 30,919 | 28,591 | -8% |

| Kerala | 1.05 | 0.8 | -24% | 16,401 | 15,237 | -7% |

| Madhya Pradesh | 3.17 | 3.23 | 2% | 49,518 | 61,841 | 25% |

| Maharashtra | 2.32 | 2.52 | 9% | 36,220 | 48,109 | 33% |

| Manipur | 0.26 | 0.29 | 12% | 4,048 | 5,630 | 39% |

| Meghalaya | 0.27 | 0.31 | 15% | 4,212 | 5,999 | 42% |

| Mizoram | 0.19 | 0.21 | 11% | 3,018 | 3,968 | 31% |

| Nagaland | 0.21 | 0.23 | 10% | 3,267 | 4,493 | 38% |

| Odisha | 1.95 | 1.9 | -3% | 30,453 | 36,300 | 19% |

| Punjab | 0.66 | 0.73 | 11% | 10,346 | 14,021 | 36% |

| Rajasthan | 2.31 | 2.45 | 6% | 36,049 | 46,886 | 30% |

| Sikkim | 0.15 | 0.16 | 7% | 2,408 | 3,043 | 26% |

| Tamil Nadu | 1.69 | 1.72 | 2% | 26,392 | 32,849 | 24% |

| Telangana | 1.02 | 0.87 | -15% | 15,988 | 16,727 | 5% |

| Tripura | 0.27 | 0.29 | 7% | 4,212 | 5,560 | 32% |

| Uttar Pradesh | 7.54 | 7.35 | -3% | 1,17,818 | 1,40,611 | 19% |

| Uttarakhand | 0.44 | 0.45 | 2% | 6,902 | 8,657 | 25% |

| West Bengal | 3.08 | 3.08 | 0% | 48,048 | 58,963 | 23% |

| Total | 42 | 41 | -2% | 6,56,046 | 7,84,181 | 20% |

Sources: Report of 14th and 15th Finance Commission (2020-21); Union Budget Documents 2020-21